Earth Day is a time to reflect on our planet’s health and the actions we can take to protect it. The 2025 Earth Day theme is “Our Power, Our Planet” and calls to promote renewable energy and energy efficiency. Here are some tips to help you save energy and lower your utility bills.

Upgrade to Energy-Efficient Appliances

Replacing old appliances with energy-efficient models can make a big difference by using less electricity and water. You can also Invest in renewable energy sources like solar panels which can lead to long-term savings on your electricity bills.

Install a Programmable Thermostat

A programmable thermostat allows you to set your heating and cooling systems to operate only when needed. For example, you can program the thermostat to lower the temperature when you’re asleep or away from home.

Seal Windows and Doors

Drafty windows and doors can lead to significant heat loss in the winter and heat gain in the summer. Sealing gaps with weatherstripping can improve your home’s insulation.

Use Cold Water for Laundry

Many detergents are designed to work effectively in cold water. Washing clothes in cold water can save a considerable amount of energy, as heating water accounts for a large portion of the energy used in laundry.

Take Advantage of Natural Light

Maximize the use of natural light during the day to reduce the need for artificial lighting. Open curtains and blinds to let in sunlight instead of turning on the light switch.

Perform Regular Maintenance

Regular maintenance of your heating and cooling systems ensures they operate efficiently. Replace air filters regularly, clean vents and ducts, and schedule annual inspections to keep your systems running smoothly.

Implementing these energy-saving tips can help you reduce your environmental impact and save money on your utility bills. By making small changes and investing in energy-efficient technologies, you can contribute to a more sustainable future while enjoying the financial benefits of lower energy costs.

Every day, Canadians across the country are targeted by scam artists. With tax season in progress, scammers may try contacting you, pretending to be your financial service provider or even the CRA.

How to protect yourself from scams Cyber security is essential in protecting personal and financial information from fraud and scams. Below are key steps to protect your wealth and stay safe:

Use strong, unique passwords. Enable multi-factor authentication (MFA) where applicable.

Be cautious with links and attachments

Never click an unverified link or download an unknown attachment

Check for spelling and grammar errors: Phishing emails often have minor mistakes.

Verify emails and web addresses

Look for small differences in URLS

Check the senders email address

Confirm who’s contacting you

Confirm full phone number – don’t trust caller ID alone

Verify identity by contacting your financial services provider directly using their official contact information

AI makes fraud even harder to identify As advancements in Artificial Intelligence (AI) have made scams more sophisticated, the risk of fraud has increased, and additional steps must be taken to recognize scams. The following are examples of AI-generated scams:

Voice cloning: Scammers can mimic the voices of loved ones over the phone claiming they need financial help.

Deepfake videos and images: Scammers can create realistic videos or images to impersonate family members or coworkers. You can protect yourself from these AI generated scams by implementing these additional tips:

Create a safe word or phrase that only close family members know which can be used to verify emergencies

Be skeptical of urgent requests

Verify unexpected calls or messages by calling a contact back using a known number to confirm

How to identify CRA scams It is important to know when to be suspicious and how to recognize a scam. The CRA website outlines how you can protect yourself against fraud. The CRA may contact you by phone, automated message, letter, or email. The CRA will NOT:

Send you refunds by e-transfer or text message

Demand or pressure immediate payments by e-transfer, Cryptocurrency, prepaid credit cards, gift cards

Threaten to deport or arrest you

Use aggressive or threatening language

Set-up an in person meeting in a public location to collect a payment

Charge a fee to speak with a call centre agent

Ask for personal or financial information in a voicemail or email

If you are unsure or suspicious:

Do not click any buttons, links, or reply to the message

Do not provide any personal or financial information

Hang up and contact the CRA directly for any tax-related manners.

There is no need to stress or worry about scams, however it is important to stay vigilant, recognize the signs and know how to respond if you are ever contacted by a potential scammer.

For further details contact a Rothenberg Wealth Management advisor.

It’s that time of year again, and you might be asking yourself, “Should I contribute to my Registered Retirement Savings Plan (RRSP) or my Tax-Free Savings Account (TFSA)?” Ideally, contributing to both is the best strategy, but if you’re forced with making a decision between the two, this article can help guide you.

Here are a few important elements to consider when deciding between RRSPs and TFSAs:

First consider your marginal tax bracket.

Start by looking at your marginal tax rate. If you’re in a higher tax bracket, contributing to an RRSP can lower your taxable income and offer a substantial tax break. In contrast, TFSA contributions don’t provide an immediate tax deduction since they are made with after-tax dollars. However, the growth within the TFSA is entirely tax-free, and withdrawals won’t be taxed either.

The second factor to consider is the contribution limit.

Contribution limits are also important to keep in mind. For TFSAs, the contribution limit is $7,000, with a cumulative total of $102,000 if you’ve been a Canadian resident since 2009 and were 18 years old at that time. That’s a significant opportunity for tax-free growth over time.

For RRSPs, the contribution limit is 18% of the earned income you reported in the previous year, up to $32,490. If you don’t use your full contribution room in any given year, it carries forward, allowing you to contribute more in the future.

Third factor and an important one, are the withdrawals.

Withdrawals are another important consideration. RRSPs are designed specifically for retirement savings, and any amount you withdraw is subject to income tax. Contributions can be made up to the age of 71, at which point you must convert your RRSP into a Registered Retirement Income Fund (RRIF).

On the other hand, TFSA withdrawals are completely tax-free. Plus, when you withdraw from a TFSA, the amount is added back to your contribution room in the following year, so you can re-contribute it later. TFSA accounts also don’t have an age limit, and there’s no need to convert it to a different account type.

Conclusion

Both RRSPs and TFSAs offer excellent opportunities for tax-free growth, but they serve different purposes in your wealth-building strategy.

RRSPs are ideal for long-term retirement savings, particularly if you’re in a higher tax bracket now. TFSAs, however, offer more flexibility and are great for both short- and long-term goals, whether you’re saving for a major purchase or looking for another option to grow your retirement savings.

The right choice depends on your personal financial situation—your income, goals, and timeline. There’s no one-size-fits-all answer, but by understanding these key differences, you’ll be in a better position to make the best decision for your financial future.

For further details contact a Rothenberg Wealth Management advisor.

In this article, we share some insights on what to expect in 2025.

Broadening Equity Market Returns

Equity markets delivered strong returns in 2024, driven by the earnings growth of a few players—the Magnificent 7, which includes Alphabet (Google), Amazon, Apple, Meta (Facebook), Microsoft, NVIDIA and Tesla. The rest of the market is expected to catch up in 2025 and deliver more balanced and diverse growth within and across sectors.

Policy Uncertainty

Economic uncertainty will be a defining theme in 2025:

With Prime Minister Justin Trudeau stepping down, the fate of important policy proposals, such as the planned increase to capital gains tax, is now unclear. The upcoming leadership transition will play a key role in shaping Canada’s future economic policies.

Trump’s proposed 25% tariffs on all Canadian exports, if implemented, could disrupt cross-border supply chains and have widespread economic ramifications, both for Canada and globally.

Interest Rates

After five consecutive interest rate cuts in 2024, Canadians can expect continued rate reductions in 2025 as the Bank of Canada seeks to stimulate economic growth. Lower rates should improve borrowing conditions, benefiting both consumers and businesses by lowering financing costs and stimulating demand.

Continued Growth of Private Markets

With many unknowns, asset classes that are uncorrelated to market fluctuations will continue to demonstrate value to investors as sources of risk-adjusted returns. In particular, lower interest rates and healthy economic activity are expected to be positive for private equity.

Conclusion

As 2025 unfolds, staying informed will be crucial to navigating an uncertain environment, capitalizing on emerging opportunities and turning potential challenges into avenues for growth.

If you would like to discuss investment opportunities and how to position your portfolio for the year ahead, contact us today and start a conversation.

The S&P 500 has experienced a remarkable surge in 2024, delivering one of its strongest performances since 1928. While past performance often fuels optimism, the critical question for investors looking at the year ahead is whether this bullish trend can sustain itself for the broader equities market.

Looking back on 2024

Year-ahead-forecasts in December 2023 about what 2024 would bring for investors were dismal, even after a year of more than 20% returns for the S&P 500. Perhaps what played a part in the pessimistic outlook for 2024 was the political uncertainty and heightened emotions of an election year.

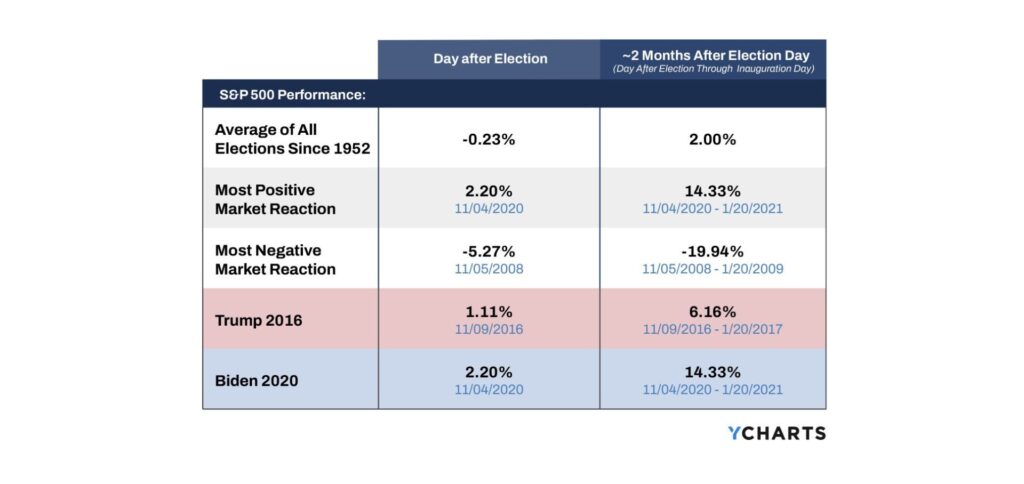

However, historical data suggests that such concerns are often overblown. The S&P 500 has not only shown resilience but posted a noticeable positive performance in 83% of election years. Any post-election losses tend to be retraced by end of year. In fact, the index generously retraces its losses, typically trading higher into the year-end and into the new year, up to two months following a U.S. election.

Figure 1: S&P 500 Performance Day After Election vs. 2 Months After Election Day

As of Dec. 13, the S&P 500 is up 27%. If it finishes up over 20%, this will represent a spectacular two-year run for the S&P 500.

Heading into 2025

Looking ahead, forecasts suggest growth potential of the S&P 500 at 9% by the end of 2025. While the outlook remains positive, the bull market could face challenges in mid-2025. Risks such as a potential economic slowdown, tightening monetary policy or geopolitical uncertainty could lead to a market pullback. And with the S&P at an all-time high currently, investors may be nervous that a market correction is on the horizon.

What does this mean for the broader equities market?

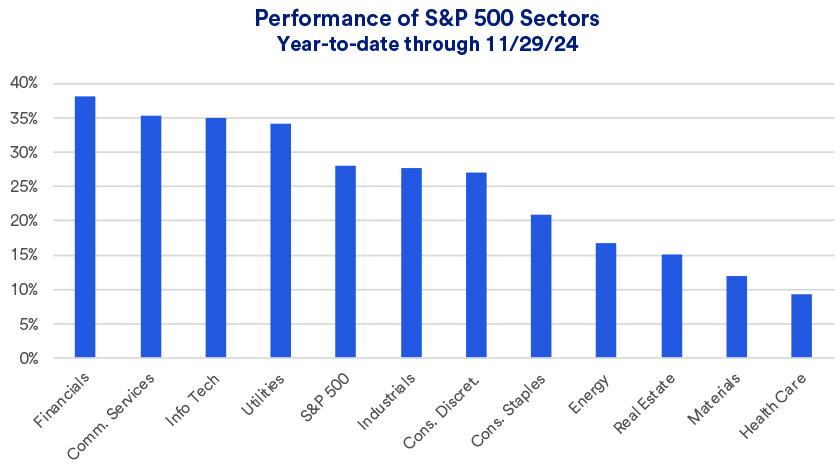

The S&P 500 is a widely used benchmark for tracking trends in the broader equities market due to its breadth and diversity. For this same reason, it provides a simplified view of market performance at best, obscuring trends within specific sectors of the economy.

Source: S&P Dow Jones Indices, LLC. As of November 29, 2024 via usbank.com

Market movements are complex and driven by a combination of factors, including but not limited to domestic and foreign policies, interest rates, geopolitical events and corporate earnings. These elements often interact in ways that make it difficult to isolate the impact of any single variable—such as an election cycle.

Recently, stocks have rallied amid expectations that tax cuts, deregulation and increased government spending will spur economic growth but the long-term impact of policies such as tariffs, foreign relations and fiscal spending remains uncertain.

The complex and unpredictable nature of financial markets means that growth may not be as consistent as projected, especially if key assumptions about policy or global conditions fail to materialize.

3 Investor Takeaways for 2025

1. Time in the market vs. timing the market

Investors should look at staying invested in the market for the long term and consider high-quality stocks. Investing in solid, well-managed companies provides a stable foundation for long-term growth, even during market dips or economic uncertainty.

2. Strategic portfolio rebalancing

Strategic portfolio rebalancing can help investors to adjust sector exposure based on changing market conditions. This helps capture opportunities in sectors with favorable valuations or strong growth potential.

3. Diversification beyond equities

Investing in other asset classes beyond equities, such as fixed income or alternative investments, may help improve risk-adjusted returns and provide a hedge against market fluctuations. This approach can potentially reduce volatility and better align a portfolio with an investor’s risk tolerance and long-term objectives.

This is an important time to connect with a wealth management professional to ensure your investments are aligned with your financial objectives and that you’re on track to reach your wealth goals. Reach out to us today—we are here to assist you in making informed investment decisions and navigating the complexities of the current market landscape with confidence and clarity, ensuring you’re well-positioned to seize tomorrow’s opportunities.

Tax-loss harvesting, also known as tax-loss selling, is a powerful strategy that can enhance the tax efficiency of your investment gains. This strategy involves selling underperforming investments and realizing a capital loss that can then be used to offset capital gains from other investments.

As a brief refresher:

Capital gains are triggered when you sell an investment for more than the price you purchased it for (profit).

Capital gains are triggered when you sell an investment for less than the price you purchased it for (loss).

Capital gains are included in your annual taxable income and taxed at your marginal tax rate. For individuals, the inclusion rate is 50% for capital gains up to $250,000 and 66.6% for the remaining amount above this threshold.

While the idea of intentionally selling a losing investment may seem counterintuitive, this can be a smart way to reduce your tax liability or in other words, the amount of taxes you owe.

Tax-Loss Harvesting Example

Suppose you purchase 100 shares of XYZ at $10-per-share, for a total of $1,000. Over time, the price of XYZ falls to $6-per share, and your 100 shares are now worth $600. You choose to sell all XYZ shares for $600 and realize a loss of $400 on your initial investment. This loss is considered a capital loss and can be applied against any capital gains realized in the same tax year, thus reducing your total taxable capital gains.

Say you also realize $2,000 in capital gains in that same tax year. Your $400 loss can be used to offset part of those gains. After netting the capital gains and losses, you would pay taxes on $800 of your earnings at the 50% inclusion rate for capital gains ($2,000 – $400 = $1,600 * 50%).

Had you not used tax-loss harvesting, you would report $2,000 in capital gains and pay taxes on $1,000 (50% of $2,000). In this example, you are reducing your reported capital gains by 20% using tax-loss harvesting.

Key Considerations

The above example provides a simplified illustration of tax-loss harvesting. In reality, most investors hold diversified portfolios with investments across account types, asset classes and sectors that require regular rebalancing and are subject to different tax treatments. This interplay can make tax-loss harvesting even more nuanced. Several other considerations should be kept in mind when tax-loss harvesting.

1. Eligible Investments

Tax-loss harvesting only applies to realized capital gains and losses in non-registered accounts. Losses within registered accounts, such as RRSPs and TFSAs, cannot be used for tax purposes, as gains and losses within these accounts are not taxed until withdrawals are made. In other words, capital losses in registered accounts cannot offset capital gains in non-registered accounts.

Alternative and private investments, such as private equity or private real estate, may also benefit from tax-loss harvesting, though challenges like liquidity, valuation, transaction costs, lock-up periods and differing tax treatments must be carefully considered.

2. Superficial Loss Rule

The Superficial Loss Rule prohibits you from claiming a tax deduction on a capital loss if you repurchase the same or identical investment within 30 days before or after the sale.

The Superficial Loss Rule is an important consideration when tax-loss harvesting, but with careful planning, you can sidestep it using strategies such as waiting 31 days before repurchasing the same investment or buying a similar but not identical investment.

3. Carry-Back & Carry-Forward Rules

Capital losses can be carried back three years or forward indefinitely to offset capital gains in those years.

For example, if you realize a capital loss in 2024, you could carry that loss back to offset any capital gains from 2021, 2022 or 2023 by filing a T1 Adjustment Request. If the loss isn’t used in the current year or carried back, it can be carried forward to offset capital gains in future years.

Final Thoughts

Tax-loss harvesting is often associated with year-end tax planning, as investors try to reduce their tax liability for the current year. However, it can be done throughout the year, especially if there are market fluctuations that create opportunities for harvesting losses. It’s important to work with an experienced financial professional like a Rothenberg Wealth Management Advisor to assess whether you can benefit from tax-loss harvesting and how you can implement this strategy to maximize your portfolio’s tax efficiency and reduce the amount of taxes owed.

Are you interested in tax-loss harvesting? Contact us by using the form below.

The new capital gains tax policy, effective from June 25, 2024, brings significant changes for individual investors, corporations, and trusts. This new policy imposes a higher tax rate on earnings from the sale of assets, like stocks or investment properties, also known as capital gains.

Capital Gains Inclusion Rate Changes

Individual Investors: Previously, individual capital gains exceeding $250,000 were taxed at a rate of 50%. However, under the new policy, these gains will now be subject to a higher tax rate of 66.67%. It’s important to note that this increased rate only applies to gains earned after the initial $250,000. The first $250,000 of gains within a tax year will still be taxed at the original rate of 50%.

Corporations and trusts: Corporations and trusts, unlike individual investors, will not benefit from the lower rate on the first $250,000 of annual capital gains. Instead, they will be subject to the higher tax rate of 66.67% right from the first dollar of gains.

The increase in the capital gains tax inclusion rate will have various implications depending on your situation. For example, the new policy may affect the timing of your investment sales, as well as the types of assets you choose to invest in. It’s important for you to understand how these changes will impact your overall tax liability and to plan accordingly.

Contact Us

If you have concerns about the new policy’s impact on your investments, we are here to help. Our team at Rothenberg Wealth Management provides free, professional advice and guidance. Our advisors can help you navigate the intricacies of the new capital gains tax landscape, understand the specifics of the policy, assess your current investment portfolio, and develop a plan to minimize your tax liability.

Old Age Security (OAS) is a source of income for many Canadians during retirement, but many retirees are concerned about losing a portion of their OAS benefits due to clawback rules that reduce these benefits after a certain income threshold. In this article, we’ll share some strategies to prevent your OAS benefits from being clawed back, allowing you to maximize your retirement income.

Before we begin, let’s review what the Old Age Security benefit is. If you are already familiar with OAS, you can skip this part and jump straight into the different strategies to reduce the impact of the OAS clawback. These strategies include:

Old Age Security is a pension benefit that provides a monthly payment to most Canadian retirees and seniors. If you meet the legal status and resident requirements for receiving OAS, you can start enjoying OAS benefits as soon as age 65 with the option to defer payments until the age of 70.

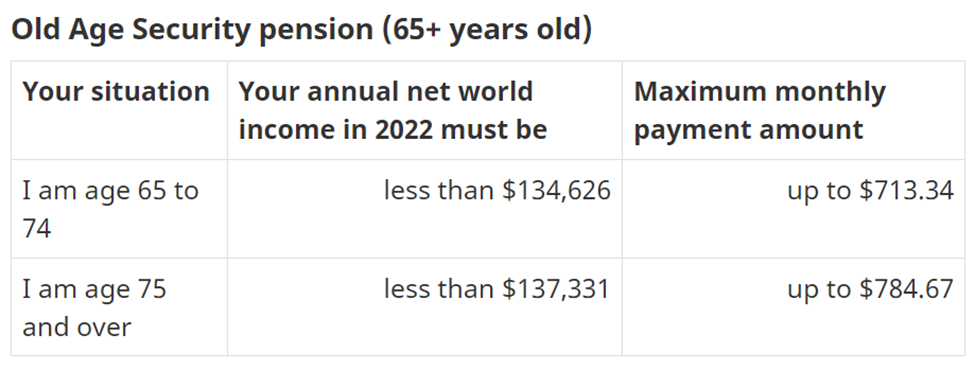

How much you will receive in OAS will depend on your income. As of April to June 2024, the maximum OAS monthly payment amount for individuals aged 65 to 74 is $713.34, and for those aged 75 and over, this amount is $784.67. These amounts are adjusted on a yearly basis depending on inflation.

It’s important to note that there is a maximum annual net income threshold for OAS eligibility. If your income exceeds this threshold, you will not be eligible to receive any OAS benefits. This is particularly relevant for high-income earners.

(Maximum payments and income thresholds – April to June 2024, Source: CRA Website)

You can find all the details about maximum payments and income thresholds (April to June 2024) on the CRA website here in addition to other relevant information about Old Age Security.

Remember, OAS is a valuable pension benefit that supports Canadian retirees and seniors. Ensure you meet the requirements and understand the income thresholds to make the most of this benefit.

Now let’s discuss the different types of strategies to manage potential OAS clawback. Most strategies presented below focus on reducing your annual net income below the clawback threshold, since this is what the amount of OAS you receive will depend on.

Income Splitting

To manage your retirement income efficiently, consider income splitting with your spouse or common-law partner. This method involves sharing up to 50% of eligible income, such as from Registered Retirement Income Funds (RRIFs) or pensions, which can keep individual incomes below the clawback threshold. It’s a strategic way to reduce your overall tax burden and effectively manage your retirement income, ensuring you receive the maximum amount of OAS you’re eligible for.

Utilizing Tax-Advantaged Savings Accounts: TFSAs and RRSPs

Early strategic withdrawals from Registered Retirement Savings Plans (RRSPs) to fund your Tax-Free Savings Account (TFSA) can be a smart move, especially if you can do so before reaching higher OAS clawback thresholds.

Another option is contributing to an RRSP if you have the available contribution room. However, it is important to note that if you are already retired and getting OAS, contributing to an RRSP may not be an option if you don’t have the contribution room or are over the age of 71. As a reminder, the last day you can contribute to your RRSP is December 31 of the year you turn 71 years old.

Another strategy involves transferring your least tax-efficient investments, like Guaranteed Investment Certificates (GICS) and bonds, into a TFSA to reduce your taxable income and minimize future tax implications. In this way, you lower your income threshold and can qualify for a maximum in OAS benefits.

Deferring OAS Payments

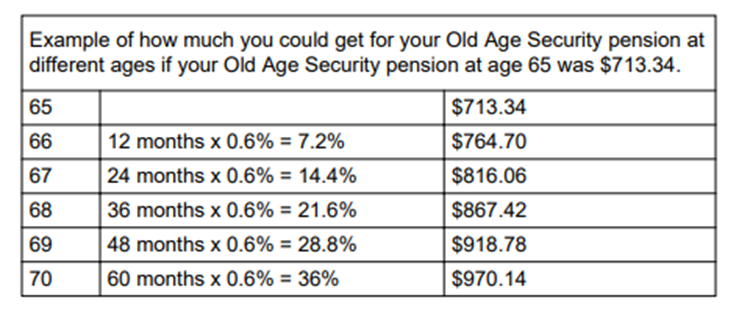

Another effective strategy you may benefit from is to delay receiving your Old Age Security (OAS) payments if you’re working past the age of 65. You have the option to defer your OAS up to the age of 70.

For each month you delay the start of your OAS pension up until age 70, your future monthly payments may increase by 0.6%. You can delay payment of OAS for up to 60 months, or 5 years, which means your OAS payments will go up by 7.2% per year up to a total maximum of 36%.

(Application for the Old Age Security Pension ISP-3550 Form, Source: Service Canada)

Delaying your OAS payments boosts your eventual payments and results in larger payments in the future but also provides a window to manage other retirement funds under lower tax brackets if you don’t need the OAS retirement income right away. You could also delay the first payment indefinitely, but there wouldn’t be any advantage.

It’s important to keep in mind that you won’t be eligible for other OAS benefits like the Guaranteed Income Supplement (GIS) and Allowance during the pension deferral period.

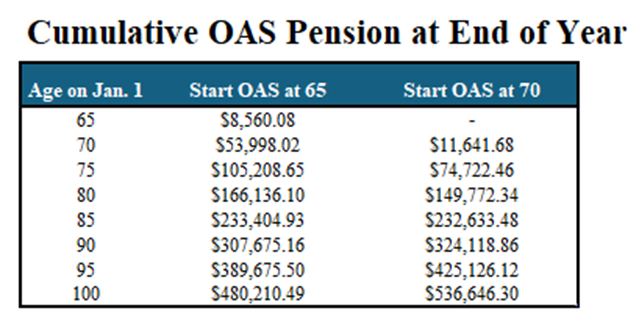

Here is a table with an estimated breakdown of OAS payments.

*This table is based on an annualized monthly maximum pension of $713.34 on January 1, 2024. Assumes conservative inflation adjustment of 2% per year on the annualized monthly pension. Adjusts pension by 10% at age 75.

One important thing to note about the table above is that it doesn’t factor in any investment returns made on OAS payments. Some people wish to take their OAS pension early and invest that money rather than delaying OAS to the age of 70.

When deciding whether to defer your OAS payments, it’s important to consider different factors besides your income requirements and the potential income boost promised to you by an OAS deferment. Other factors you may want to consider include your health and any dependents.

Flow-Through Shares (FTS)

Another viable option to minimize your OAS clawback is to invest in Flow-Through Shares, or FTS. FTS can give you a tax deduction to reduce your taxable income. These types of investments are not for everyone as they can carry high risk, which can lead to significant losses, so it’s important to speak to your advisor to know if this option is suitable for you.

Other Strategies

Consider other financial planning strategies such as reallocating income to reduce or eliminate the clawback of OAS benefits. For instance, reallocating eligible pension income to enable both spouses to receive the pension income tax credit can be beneficial.

Additionally, waiting until the end of the year you turn 71 to convert your RRSP to a Registered Retirement Income Fund (RRIF) and taking only the minimum RRIF withdrawals annually can keep your net income low.

Prudent investing is also important along with understanding how different income is taxed. Not all investment income is taxed the same, so it’s important to select investments that are tax-efficient, which an advisor like a Rothenberg Wealth Management Advisor can help you with. This can also mean rearranging or rebalancing your portfolio to continue generating the income that you need but also change the type of income you receive from interest, dividends, or capital gains to return of capital, to further reduce your taxable income in a given year. Return of income capital, or ROC, is not taxable in the year it is received.

Applying strategies like income splitting, utilizing Tax-Advantaged Accounts like TFSAs and RRSPs, and opting to defer OAS payments until you turn 70 years old can be practical steps that can safeguard your income in retirement, ensuring you maintain as much of your OAS benefit as possible. Remember, every financial decision you make impacts your retirement comfort, so planning with these strategies in mind is critical.

The journey to maximizing your Old Age Security doesn’t have to be navigated alone. Whether you’re fine-tuning your current retirement plan or just starting to ponder over your future finances, professional advice can make all the difference. Contact a Rothenberg Wealth Management Advisor for retirement planning advice to explore how you can implement these strategies effectively in your overall wealth management plan.

Founded in 1986, Rothenberg Wealth Management is a leading investment firm and trusted wealth management partner for families, individuals, their affiliated business and condominium corporations.